|

Mar 24

Why Climate Change Is Going to Wreck Our Financial System

What Happens When You Don't Build a 21st Century Economy? This Does

By now, you can see: it's not over. What began with Silicon Valley Bank and Credit Suisse is still intensifying. "Jitters," as they say, are racing through the financial system. What's all this really about? Why, suddenly, do we seem to be poised on the edge of a banking crisis — out of the blue?

Polycrisis. It's a word we should all know. The world emerges from a pandemic — and plunges straight into a banking crisis. And you're quite right to remonstrate that, no, Covid's not "over" — we just pretend as if it is. We race from, it seems, one crisis to the next. Why? What's going wrong?

Let me answer the question that's probably on your mind. Are we headed for another banking crisis? Yes, most likely, we are. It's inevitable, in fact, just a matter of time. Not in the usual sense — cyclically. But in a secular sense. We are headed for the mother of all financial crises — and I want to explain in a little more detail just why. If you want the summary now, it's about the end of the Industrial Age, and the Dawn of the Age of Extinction, or, in a less accurate sense, "climate change."

Our financial system isn't fit for this century, and until it is, it's going to be hit by intensifying crisis — just like the rest of our systems, from food to water to energy to healthcare. What do I mean by that?

There are two kinds of banks. Retail banks and investment banks. Retail banks hold your deposits and lend to households. Investment banks…invest, or at least so the theory goes.

How is this financial system coping with…the Age of Extinction? It's not.

Now. What's going on in the economy? Well, prices have soared, and real incomes have fallen. People have gone further and further into debt. Meanwhile central banks keep on raising rates, to try and tamp down prices, but it's not working, precisely because it's not about too much demand, but too little supply — the world's running out of water, food, energy, our planet unable to supply us with the basics at the old levels. So we can see, easily, that a certain chain of consequences is likely to ensue. Price go on rising — do you think the planet's going to magically spirit up more water, clean air, food? People can't make ends meet. Interest rates keep on rising. Plenty of the debts people are in just to make ends meet they're in go bad. Bang. Banking crisis.

The precise mechanism doesn't matter so much. Is it mortgages people can't pay? Credit cards? Car payments? All of the above? Our financial systems is a maze of "derivatives" — secondary bets — on various forms of debt. What matters more than the precise form of trouble is understanding the point: risk is now accumulating in the system that it can't handle. People are stretched to the limit already, but prices are only going to rise, and so are interest rates, and that means that almost certainly banks will be hit by waves of bad debt.

Let's zoom out for a second and think now not like bankers, but economists. What's happening here at a macro level? Living standards rose for centuries, after the Big Bang of the Industrial Revolution — but that ascent has now come to a halt. Not my opinion, empirical fact. Living standards have fallen in 90% of countries. Now we are in a new and very different economic age. To maintain the same living standards as we took for granted during the Industrial Age, we will have to pay more and more, because scarcity is the great trend of now. Having hit the planet's limits, every drop of water, meal, joule of energy, and so forth, will cost more and more — at least until we reinvent our basic systems for them. Those systems are still — all of them — Industrial Age ones. They were not meant to cope with scarcity, and now that limits have been hit, planetary ones, they can't provide the same level of abundance. Do you see how different the economics of the Age of Extinction and the Age of Industry really are?

In this gap there's all but certain to be the mother of all financial crises. Because our Industrial Age economies cannot provide the same living standards as we took — and take — for granted, except at higher and higher prices, which, of course, mean everything from bad debt to bankruptcy to interest, all of which have to be absorbed by banks, and will inevitably crush some, perhaps many.

Now. The key phrase in all the above was: "until we reinvent our systems." Prices will just keep rising. For everything — food, energy, water, healthcare, etcetera. How much more are you paying for all these things already? I'm sure you're feeling the pinch — we all are. This is what falling real incomes means. Our living standards are now declining as a civilization, and another way to say that is: what we once took for granted is becoming unaffordable. Until we reinvent our systems.

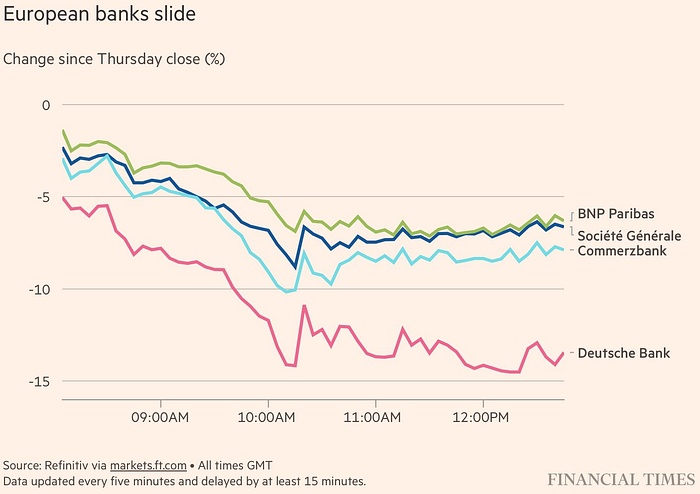

That brings me to the other end of banking. Investment banking. How's that doing? Well, let's think about it. Yesterday, it was Silicon Valley Bank and Credit Suisse that went down. Today, multiple banks are being hit by jitters, from regional American banks to Deutsche Bank, the German giant. Why is this? Is it just about confidence and liquidity and other assorted forms of jargon? Nope. It's much, much simpler to understand, if you think about it.

What are investment banks there to do? Invest. But of course we all know that they don't. At least not in anything much useful, anyways. They basically put together deals for hedge funds and private equity funds to asset strip once proud institutions, or maybe float IPOs for today's whack-job IPO. They'll throw money at apps and get-rich-quick schemes. They'll back privatized utilities which fleece people an arm and a leg for…insulin. You know the score, which is why "investment bank" is a term that people laugh at with contempt. They don't invest, really — they play roulette with other people's money, and then we have to bail them out.

Now. That was the story of financial history to date, but in fact, now, it's worse. Take a hard look at the economy again. Remember what we need? To reinvent our systems. That is what investment banks should have been doing. But we're nowhere close. I mean we're so far off the mark that it's laughable, really. Let's go back to the IPCC's list of systems we need to reinvent, which is something everyone should know, if not memorize.

There are feasible adaptation options that support infrastructure resilience, reliable power systems and efficient water use for existing and new energy generation systems (very high confidence). Energy generation diversification (e.g., via wind, solar, small scale hydropower) and demand side management (e.g., storage and energy efficiency improvements) can increase energy reliability and reduce vulnerabilities to climate change (high confidence). Climate responsive energy markets, updated design standards on energy assets according to current and projected climate change, smart-grid technologies, robust transmission systems and improved capacity to respond to supply deficits have high feasibility in the medium- to long-term, with mitigation co-benefits (very high confidence).

Investment banks should have been putting investment into all of that stuff. But they haven't been, and so we don't have any of that stuff yet as a civilization. The situation's so absurdly bad that we have…a handful of green steel plants. No real replacement for plastic. No idea how to make fossil-fuel free food, water, or energy at a civilizational scale.

Now. When I say that investment banks should have been investing in this stuff, I'm not just moralizing. I'm making an economic point. Why should they have been investing in this stuff? Because the rest of the stuff? The Industrial Age stuff? It's going bad. It's all past its sell by date. Let's take a simple example. You pour money into some app. You make a few bucks, or maybe the stock tanks. Risk. You pour money into a privatized healthcare company. You make a few bucks, but guess what, you're plagued by increasing levels of bad debt. You "invest" in private prisons, and hey, you reap a bit of a fortune, but what was the opportunity cost? You didn't invest in stuff that was going to do far, far better, over a longer time horizon.

Maybe you see my point. Investment banks have not been investing in the very things that our economies need. Systems and institutions for the 21st century. That's foolish for them. Because now their books are full of stuff that's…going bad. Going to keep going bad. From apps to privatized utilities to get-rich-quick stocks. Their books are full of Industrial Age stuff. But what's happening in the economy? Our living standards are falling. People can't afford that stuff at the same levels. Bad investment. It's not going to yield the returns you wanted it to. And now the risks are mounting.

What kinds of risks? Civilizational risk. It's made of climate risk. The risk of another pandemic. The risks to democracy, as living standards fall. Sudden destabilizations and fractures, in society, politics, supply chains, all of it. Having books full of Industrial Age stuff? It's a recipe for that risk to suddenly come due.

Now imagine the opposite scenario. Investment banks had actually…invested. In stuff the entire world needs. Green agriculture. Clean energy. Closed loop manufacturing. Just think of all the stuff on the IPCC's list. How much better an investment would all that have been? Incalculably better. Books full of all that stuff? They'd be safe. Far less risky. Sure, the returns might be less now, than investing in some dystopian garbage, private prisons, AI, deepfake apps, whatever, but over time? They'd absolutely crush. Over decades, a century? You'd have earned far, far more — by orders of magnitude, and you'd have done so at far less risk, too. Sure thing.

But investment banks haven't done that. Any of it, really. Maybe a few, here and there, have a tiny, tiny amount of clean energy in their portfolios, but that's about it. By and large, though? Their investments are all Industrial Age stuff. And those are going bad. What "our basic systems are failing" means is precisely that those investments are failing, too. They are not going to survive. All of these are what are referred to sometimes as "stranded assets." That refers to oil and gas investment, but the problem is larger. When you have a portfolio full of Industrial Age stuff…on a dying planet…where people are getting poorer, fast…and living standards are falling…good luck surviving as a bank. Those investments will flame out — it's just a question of precisely when.

Those investments are already beginning to fail. Take a look at the tech industry. Now that it's in trouble, it's spinning AI as the Next Big Thing. The problem it faces, though, is much simpler. Living standards are falling. The tech industry basically exists on ads at this point. But when people are getting poorer, guess what, there's less point in advertising, and so advertisers have cut back. Cue wave after wave of tech layoffs. The hype about AI disguises this point. But this is an example of the larger theme, problem, issue. As living standards fall, investments in Industrial Age systems — even later ones, like tech — will turn out to be bad bets. Because people can hardly afford the basics, and that problem will only get worse. Can you eat that app? I didn't think so.

Let me give you another example. In the financial industry, Credit Suisse and Deutsche Bank have for some time been something of a running joke. Why? Ask anyone in the know, and they'll tell you, with a raised eyebrow, that their portfolios…are…dubious…sketchy…not of the highest quality. To translate that into plainer English, they'd become something of a running joke for financing the world's least savory people. Hiding their money. Piling it up offshore, and then pumping it into shady property deals, or lord only knows what. Talk about stranded assets.

You can play that game — being a banker to war criminals, to caricature the situation slightly — but what happens when people suddenly start to look, seriously, at the quality of your investments? How sound they are over the long run? Whether they can be made good on even as living standards fall? How safe and secure they really are? Now that war criminal owns fifty buildings in cities around the world — but guess what, people can't pay the rent. He owns, through some shady "vehicle," 30% of some equally shady app, cryptocurrency, company, fund — that's now going broke. Good luck with that kind of portfolio in a global economy that's suddenly effectively shrinking. This is why contagion is spreading through the system — there's a flight to quality. And had these banks invested in things that mattered, systems for the 21st century, not just hiding dubiously gained money and then putting into even more dubious, dying Industrial Age stuff, they wouldn't be going under.

So. We've discussed ways in which we're headed for a banking crisis — let me sum them up, because that's a lot to take in. On the retail side, as prices rise, and interest rates soar, people are going to be unable to pay their debts, already stretched to the limit — and that's certain to hit banks. On the investment side, investment banks haven't invested in any of the systems we need for prices to fall — which is foolish for them, because their books are now full of stranded Industrial Age assets.

There's a wrinkle in this story, of course. Sure, there's going to be profiteering. There already is. Half of inflation right now is going to straight to profit margins, which are the fattest in modern history. But being able to profiteer doesn't make a good investment. It just makes a quick buck, and these things are different. Profiteering now, as people's living standards are plummeting, might seem like a good idea. But is it? You can only do it for so long, and the more corporations profiteer — which, LOL, investment banks think is a great idea — the poorer people get…and the quicker all those debts go bad. In other words, here we have a vicious cycle at work. Don't mistake profiteering for "no financial crisis." In fact, runaway profiteering is often how financial crises happen — just think of 1929. In this day and age, profiteering accelerates risks — it's a mechanism which puts the "poly" in polycrisis.

Are we headed for another financial crisis? My friends, we're already in one. It's one facet of the age of polycrisis, as inevitable as crises in everything from food to water to healthcare to democracy. It happens a bit later, because banks absorb the risks and costs of all these crises — which are now mounting to a degree that they can't afford. Banking crisis? Already here. Some of us just don't know it yet.

Umair

March 2023

No comments:

Post a Comment